Taste Gourmet (8371 HK)

A capable operator in a tough industry

Before we dive into today’s topic, it is important that we reiterate the purpose of this blog. Investing is a lonely journey, more so for a value investor. We hope we can make this journey a little less lonely - by connecting like-minded people and discussing the companies we find interesting. We are not here to pitch any stocks and to make any investment recommendations. Our analysis is not meant to be the most detailed, for fear of boring most of the readers. So do not hesitate to comment below, or ask questions. There are always more we can share!

With that out of the way, let’s dive into Taste Gourmet, a catering group listed in the secondary market (or GEM board) of the Hong Kong Stock Exchange.

Catering is usually a business with little moat, characterised by low barriers to entry. While some brands are widely recognizable, humans generally want to devour something different each day, therefore it is an everyday struggle for restaurants to stand out among competition. Having said that, we think Taste Gourmet is a very adaptable and capable operator, allowing it to survive better than its competitors.

If one look at Taste Gourmet’s IPO prospectus back in 2017, it had 14 restaurants under 7 different brands, but 10 of those restaurants were under 3 particular brands, namely Nabe Urawa (Japanese hot pot), La’taste (Vietnamese), and Dab-pa (Chinese (Peking & Szechuan)), and the plan was to open 8 more outlets under these brands funded by the IPO proceeds. After all, it would be a usual strategy for a restaurant operator - find a working concept and expand as much as you can.

By mid-2023, these 3 brands only account for 17 out of 42 restaurants it is operating, and the ratio looks set to decrease further, considering the pipeline of restaurants that will be opened soon. It currently operates an astonishing 19 different brands, broadly falling under 4 different cuisines.

What happened was Taste Gourmet slowly transitioned itself into a mall-owner solution provider.

In Hong Kong, a restaurant can either operate in street-level shops or commercial buildings, usually owned by individual investors, or in malls, usually owned and operated by major developers. Individual landlords do not care who the tenant is as long as rent is maximised and collectible. Rent is usually fixed for at least 3 years, as individual landlords usually do not have the resources to implement turnover rent, posing significant fixed costs to restaurants. There is also no control on competition. A similar cuisine could spring up nearby any day and compete away your business.

In contrast, mall owners value foot traffic, and a good tenant mix is essential. Rarely one can find multiple restaurants of the same cuisine and price range in a well-operated mall, reducing competition for a restaurant operator. The rent is usually a percentage of turnover with a fixed minimum. As long as a restaurant achieves the turnover rent threshold and helps draw traffic to the mall, mall owners usually have little incentives to replace them in search for slightly higher rents, for fear of harming the tenant mix and risking negative impact to foot traffic.

Indeed, the first few restaurants Taste Gourmet opened back in 2007 - 2010 were street shops. It then found out upon expiry of the leases, the landlords had a lot of bargaining power. It coincided with a period where rent for street shops were skyrocketing, driven by widespread opening of retail shops targeting the ever-increasing and high-spending Chinese tourists. Taste Gourmet realised they had to transition and adapt.

It decided to open new restaurants only in well-operated malls. Being customer-centric, Taste Gourmet had to adopt a completely different mindset to truly cater to the needs of mall owners. Instead of the product-oriented strategy of a typical catering group - find a suitable location to expand your brands, mall owners prefer a location-oriented strategy- find a suitable product for a particular location. A typical store opening process for Taste Gourmet does not start with thinking how they can expand their existing brands, but by evaluating collaboratively with mall owners what suits that particular mall and its shoppers. In some cases, they are willing to tailor-make new F&B concepts or brands, as mall owners seek to provide new and differentiated experiences to customers. This is why Taste Gourmet manages 19 different restaurant brands.

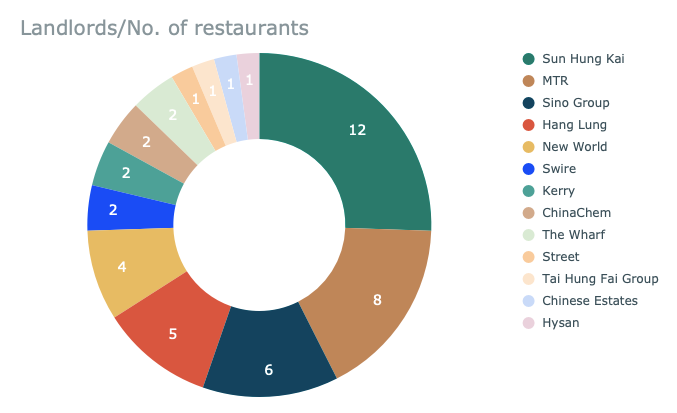

Given the orientation of the business is completely focused on the needs of the malls and their owners, Taste Gourmet manages to build and maintain excellent relationships with the mall owners. An objective measure of relationships with mall owners is the number of restaurants located in the same malls and under the same landlord, indicating trust by mall owners and ability to execute different dining concepts.

We think the implication of the above is that it significantly de-risks the company:

Increasingly Taste Gourmet is working with the same mall owners and opening more restaurants within the same malls. We think this increases the chance of success given better mutual understanding: a) mall owners understand Taste Gourmet’s brands and capabilities and therefore can better match location with dining concept, and b) having operated in the same malls, Taste Gourmet have a better understanding of the customer base and their preferences.

Ability to innovate and open new dining concepts or brands means they can replace ageing or underperforming brands. In fact, they have closed down a couple underperforming restaurants in the past and replaced them with another cuisine in the same location (of course, subject to approval of mall owners), and successfully turnaround those stores. Its ability to pivot improves the longevity of the business by extending its life cycle, and therefore reducing the downside for investors.

Well-operated malls have strong traffic, effectively guaranteeing some revenues, and also reducing the need of marketing dollars.

Its success is not dependent on a dominant brand.

Its operating environment inside malls are relatively less competitive.

Rent is more predictable in malls and their restaurants have lower risk of relocation. Store opening costs as a result of relocation can take years to recover, depending on the success of the new location.

Benchmarking other listed catering groups in Hong Kong also reveals Taste Gourmet is a very capable operator. The chart below shows Taste Gourmet earns industry-leading margins.

Management

We think besides the better economics mentioned above, its founder management - Mr. Wong and Ms. Chan, a couple, also take credit. They are accountant and math teacher by training respectively, and according to our conversation with employees, they are sharp with numbers, very hands-on, and laser-focused on all costs.

It is a common practice in Hong Kong for major shareholders to pay themselves a huge dividend prior to IPO, so that the cash is not “shared” with minority shareholders. Mr. Wong and Ms. Chan, however, chose not to do so, and cash was retained in the listing entity. During the pandemic, they also decided to skip a dividend payment, because they didn’t want to benefit themselves, while the employees had to risk their health at work and some took unpaid leave during lockdowns. We feel the management treats people fairly and are not looking to benefit themselves only.

Valuation

The stock currently trades at 7% dividend yield (at the price of HKD1.44), and likely will continue to grow. Another 10 restaurants are expected to open in Q2 to Q3 2023. It is highly cash generative and has over HK$ 100 million of cash on the balance sheet, against a market cap of $540 million, and management targets to achieve earnings of HK$ 100 million in the coming year, equivalent to a P/E of 4.4x on ex-cash basis. Payout ratio is currently below 60%. As cash continues to accumulate, there might be pressure to increase payout in the future. Below is our attempt to forecast, taking into consideration management’s plan and apply a little bit of discount.

One potential reason for undervaluation is due to its GEM-listed status. Due to more relaxed listing requirements compared to the main board, the GEM board largely consists of companies with questionable quality and integrity, and are generally shunned by investors.

Conclusion

We think there is still a lot of runway for the company, considering there are still good malls it has yet to penetrate. There is also room to open more restaurants in some of the same malls. Having said that, we will keep a watchful eye on whether it is a scalable business model - it is a daunting task to operate so many different brands. There is also key-man risk. Relationships with mall owners rest with its founders, as well as its operational excellence.

Disclosure

The author of this article owns shares in Taste Gourmet (8371 HK).

This article is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities mentioned herein. Readers should conduct their own research and due diligence before making any investment decisions. Investing in stocks involves risks, and past performance is no guarantee of future results. The author assumes no responsibility for any losses incurred as a result of using this information.

The views and opinions expressed in this article are purely those of the author and do not reflect the official position of any organization they may be affiliated with. The author has not been compensated in any way by any of the companies mentioned in this article. Please note that the author may buy or sell shares of any of the companies mentioned in this article at any time without further disclosure.

Wonderful write up. Thanks for sharing this.

A quick question - How do you connect with investors from other jurisdictions & collaborate with them for corporate governance checks etc.? I ask this because quite often I face difficulty in connecting with a reliable investor of the area to have a ground level understanding of the company & the management.

Glad I found your substack, I didn’t realize there was a write up on Taste! Nice work!